The Accommodation Pricing Review landed on 22 April, and the funding year turns over on 1 October. Most providers are still working through what it means for them, and understandably so. There is a lot in the package.

At our webinar last week we focussed on the part of the picture we think is being underweighted: not the headline AN-ACC number, but where the margin that funds your future actually comes from.

The headline is only half the story

IHACPA has not yet released its 2026–27 pricing advice, but the inputs are clear enough to model with some confidence. Our expectation is a price increase of between 3.5% and 4.5%, lifting the base from $295.64 to somewhere around $306 to $309 per NWAU. The Fair Work Commission lifted modern award wages, and a further aged care work value increase for nurses takes effect in August. With direct care running at roughly two-thirds of cost, those rises are hard to absorb under a lift of about 4%. IHACPA prices to efficient cost rather than raw wage growth, which is what holds us below the top of that range.

The more important point sits underneath the number. The latest cost analysis shows a misalignment between current AN-ACC funding and the actual cost of delivering care, across both resident classifications and Modified Monash regions. Some classes are funded above the cost of care; others consume a higher share of subsidy and may need uplift. The base care tariff is likely to tighten for MM 2 to MM 5.

The practical consequence is that a 3.5% to 4.5% increase will not reach every provider equally. Two homes can receive the same headline indexation and land in very different places once class weightings and base care tariff changes flow through. That gap between headline price and net funding is only visible through your own claim profile.

Care is becoming a break-even proposition

Here is the figure that reframes the conversation. On an average daily subsidy of $294, built on a case mix of 215 care minutes including 45 registered nurse minutes, our modelling leaves a surplus of about $16 per resident per day once staffing, clinical needs, consumables and administration are met. That is roughly 6%, and only if you deliver exactly 100% of your care minute target.

The same resident in a modelled $480,000 room generates closer to $40 per day, or around 24%, once accommodation costs are accounted for. That is roughly four times the margin care subsidy can return.

We are not saying chase profit. Even straightforward cost recovery has to carry depreciation, refurbishment and the surplus that reassures lenders and attracts investment. But the implication is hard to avoid. If care subsidy is priced to efficient cost, the operational surplus that funds quality, reinvestment and growth increasingly has to come from accommodation and other non-care revenue. And underspending on care to manufacture a margin is no longer viable, because missing your care minutes will soon reduce your subsidy.

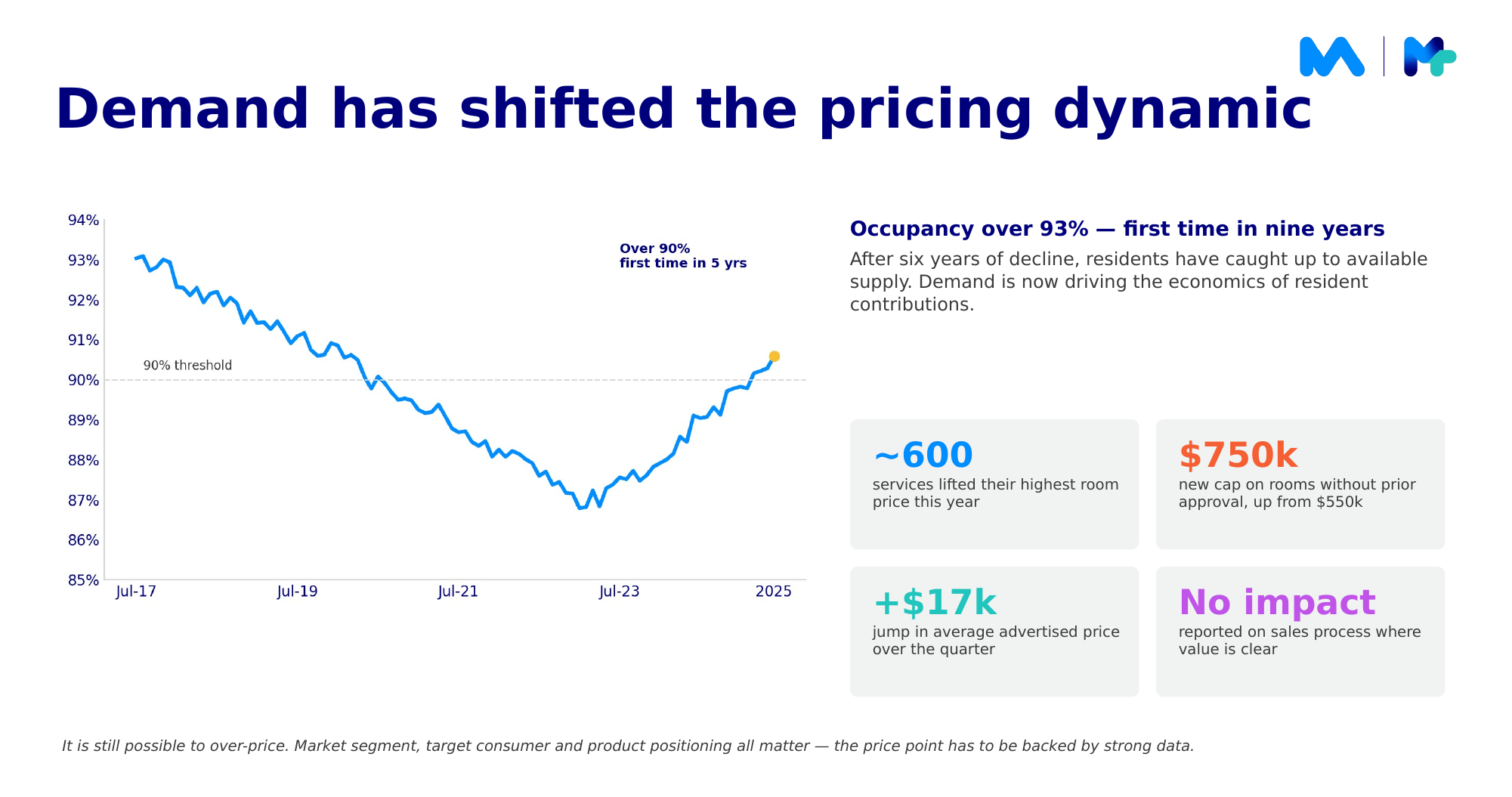

Demand has changed what is possible

The timing matters because demand has shifted. Occupancy has tipped over 93% for the first time in nine years. After six years of decline, residents have caught up to available supply, and that has changed pricing behaviour, particularly since the maximum room price without prior approval rose from $550,000 to $750,000. Providers across the sector have lifted prices, and many report consumers accepting the new points where the value proposition is clear. It is still possible to over-price, of course. Market segment, target consumer and positioning all matter, and the price point has to be backed by strong data.

The levers worth modelling now

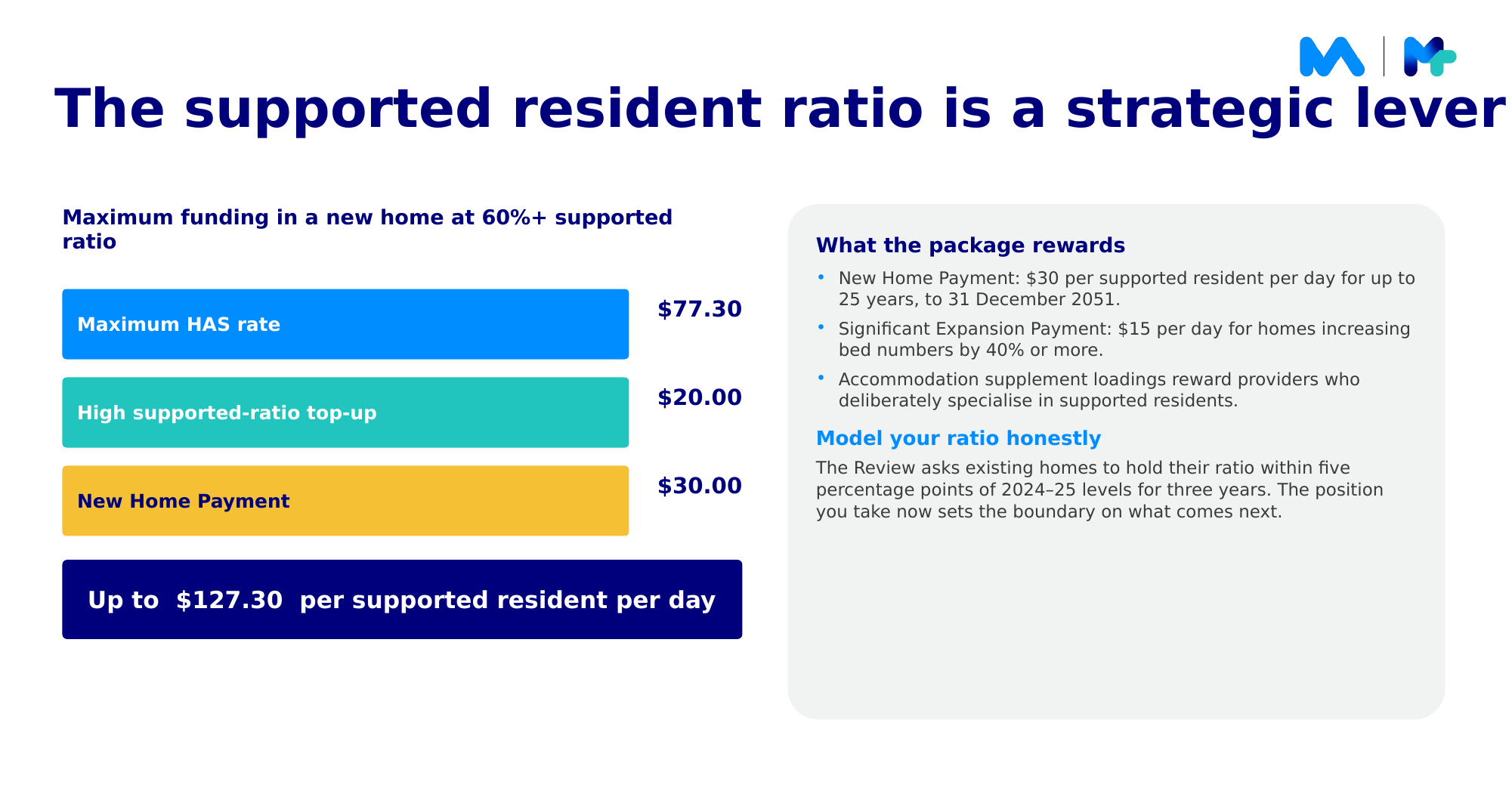

From 20 March next year, subject to indexation, the government’s response to the Review restructures the Accommodation Supplement: a new middle tier of the higher supplement at $66, the three lowest tiers removed with the base set at $52, and a new $20 per day top-up for homes with a supported resident ratio of 60% or higher.

Together, those loadings turn the supported resident ratio into a genuine strategic lever. In a new home at a 60%-plus ratio, the maximum higher supplement of $77, the $20 top-up and the $30 new home payment could total up to $127 per supported resident per day. A significant expansion payment of $15 per day is also available for homes that increase bed numbers by at least 40%. There is a commitment attached, though: existing homes are expected to hold their ratio within five percentage points of their FY25 level for three years. The position you take now sets the boundary on what comes next, which is why we would model that ratio honestly rather than optimistically.

The constraint, for many, is capital. New financial and prudential standards under the new Act are expected to lift liquidity requirements materially, and liquidity is already highly variable across the sector. The demand is coming regardless, and meeting it will take both refurbishment and genuine expansion.

What we would take to the board

Three questions worth putting on the next agenda. Have we stress-tested our accommodation pricing against the post-Review settings, especially if our rooms are still anchored to the old $550,000 threshold? Do we know our supported resident ratio well enough to plan around the new loadings and the three-year commitment? And have we re-tested the capital decisions evaluated under the old regime, the land sales, exits and refurbishments?

This is the work we do alongside providers: connecting funding, care minutes and roster data so you can see what each scenario means before it happens, class by class and home by home.