When the Accommodation Pricing Review landed on 22 April, our read was straightforward. The package hands out no across-the-board uplift. It rewards active managers. An established home trading at break-even will not see a meaningful change in revenue without deliberate action.

Two months on, we put that to the test. At our June webinar we ran four polls, drawing between 183 and 190 responses from around 170 organisations. Taken together, they give us one of the clearest reads we have on where the sector actually sits.

The short version: most providers are still waiting.

Two months on, most have not moved

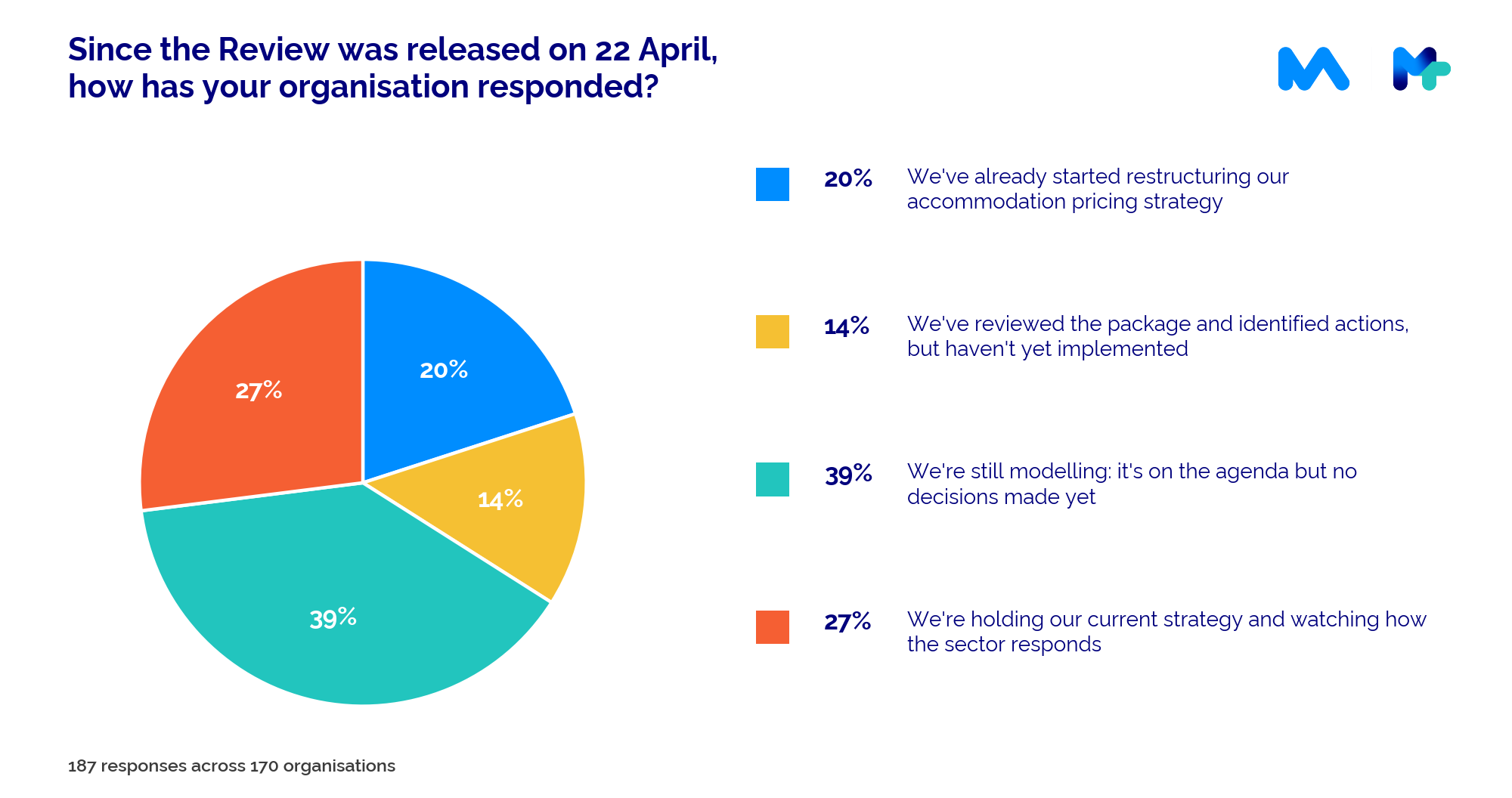

We asked how organisations have responded since 22 April. One in five have started restructuring their accommodation pricing strategy, and a further 14% have reviewed the package and identified actions without yet implementing them. That leaves two-thirds either still modelling with no decisions made (39%) or holding their current strategy and watching how the sector responds (27%).

None of that is unreasonable on its own. The Review is dense, the settings phase in from 20 March 2027, and modelling before moving is what we would suggest. But watching the sector only works if someone in the sector moves first, and right now 66% are watching each other.

Confidence is the harder number

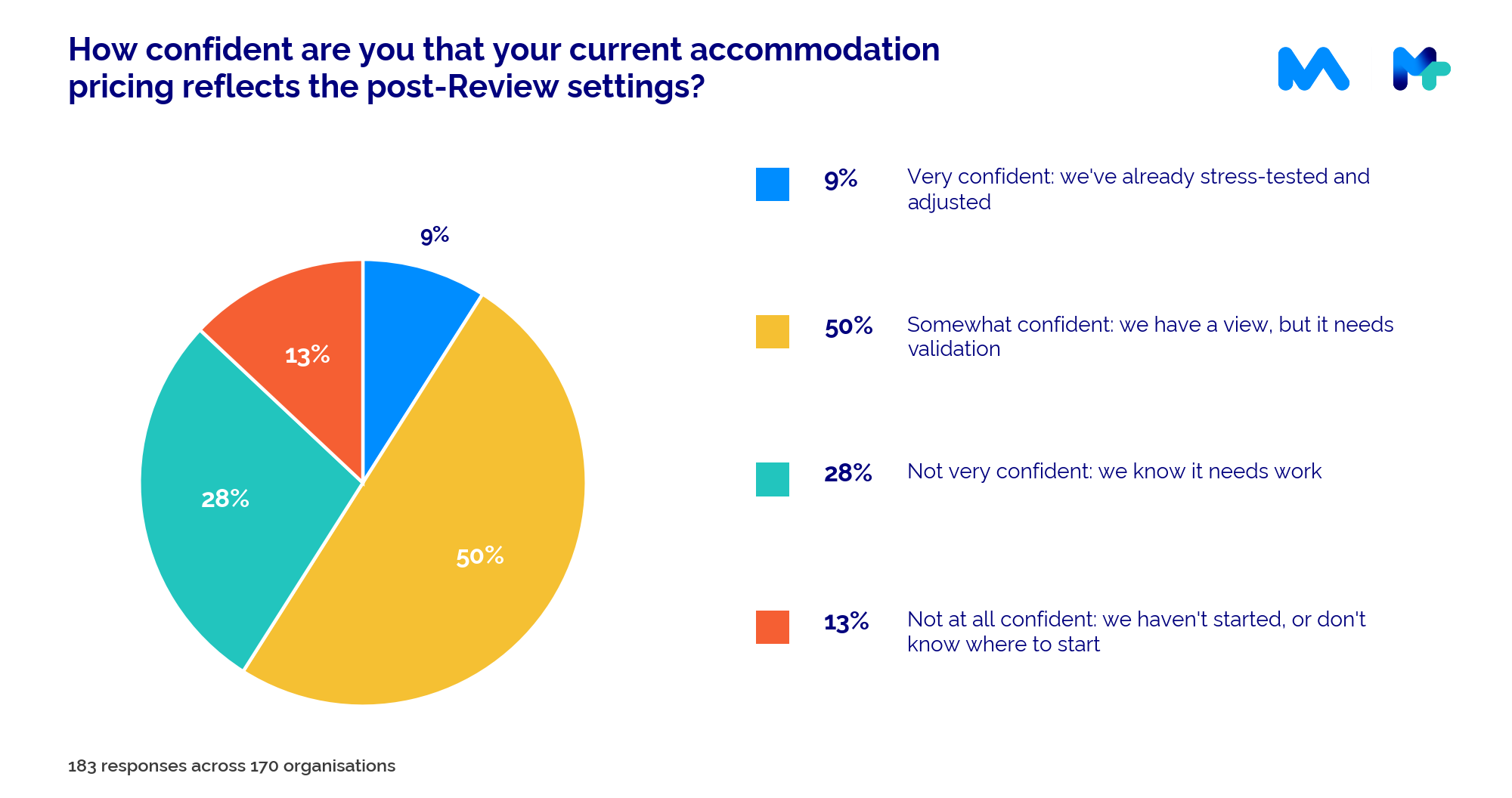

The response question tells us what providers are doing. The confidence question tells us how they feel about where they already are, and it is the starker result.

Only 9% are very confident their current accommodation pricing reflects the post-Review settings, meaning they have already stress-tested and adjusted. Half have a view but want validation. And 41% openly say their pricing needs work or they do not know where to start.

Put the other way, 91% of the organisations that answered are not fully confident their room pricing reflects the new rules. With the four-year reapproval cycle going, the price-cap framework shifting to a DAP basis and conversion rates opening up, pricing set under the old regime is carrying assumptions the new one does not share.

The money and the levers point in different directions

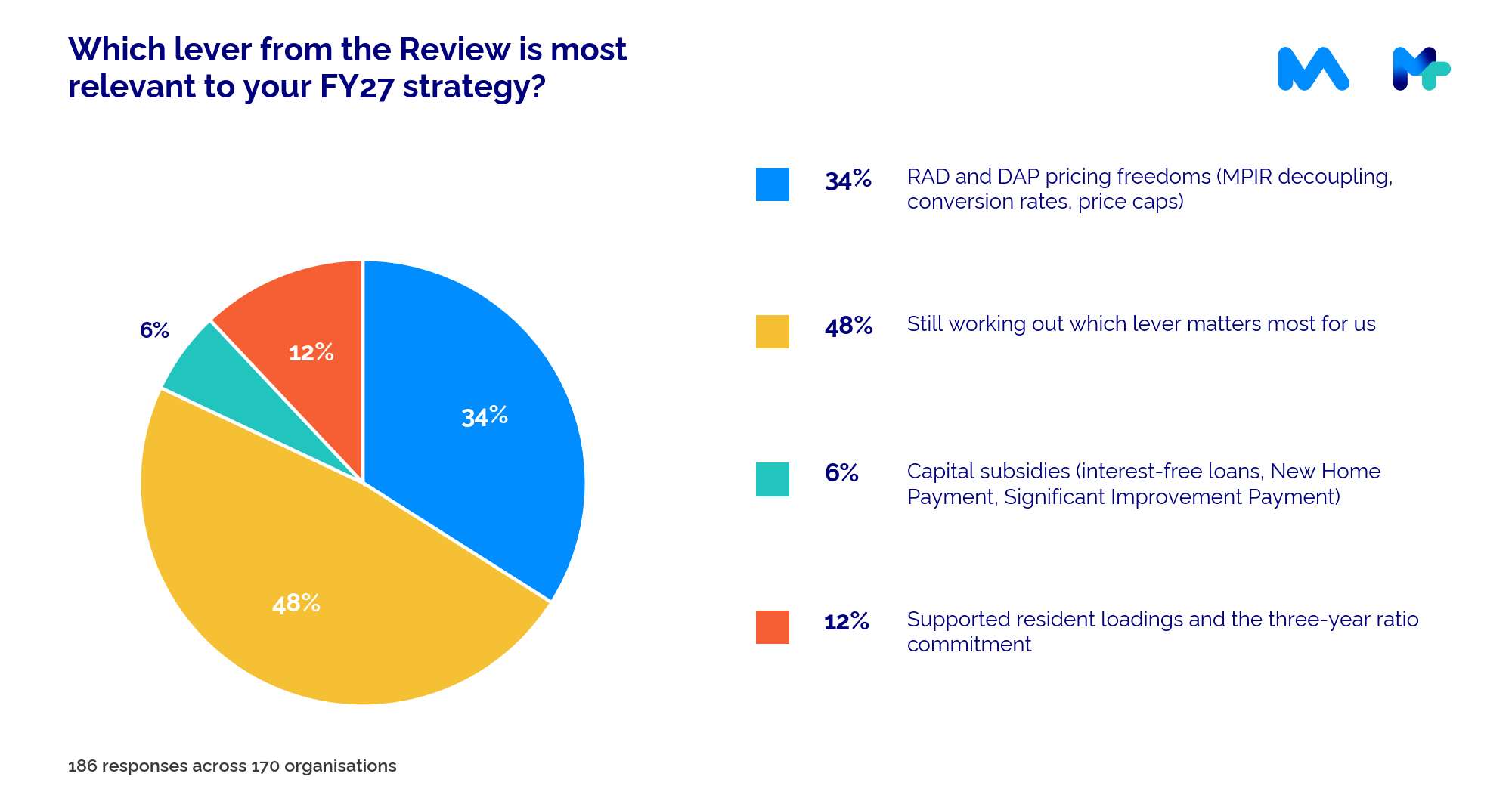

Here is the finding we did not expect. The Government's initial response to the Review leads with capital: the New Home Payment, the Significant Improvement Payment, the restructured accommodation supplement, and consultation on the Review's recommended interest-free loan scheme, all part of a $3 billion package aimed at 5,000 new beds a year.

Yet when we asked which lever from the Review is most relevant to FY27 strategy, only 6% of providers named the capital subsidies. More than five times as many, 34%, pointed to the RAD and DAP pricing freedoms: MPIR decoupling, conversion rates and price caps. Another 12% chose the supported resident loadings and the three-year ratio commitment. And 48% are still working out which lever matters most for them.

That gap is worth sitting with. The headline dollars are flowing to supply, but providers see the near-term action in pricing settings that cost the Commonwealth comparatively little. Both can be right. Capital rewards a small number of providers building or significantly expanding; pricing freedom touches every provider with a room to sell. The poll suggests the sector already understands the difference.

Expectations follow effort

The last poll asked what impact providers expect the package to have on their FY27 revenue position. Only 11% expect to be a meaningful beneficiary. The largest group, 37%, expect to recover some upside with focused work. Meanwhile 29% expect the package to largely pass them by without action, and 24% are worried they will be worse off or cannot yet see the impact.

Notice the wording that respondents chose for themselves. The optimists condition their upside on focused work, and the neutral group expects to be passed by without action. Either way, the sector is telling us the same thing we said in April: the outcome depends on what you do, not on what the package does.